Market and Asset Allocation Update – April 2026

CiN-sights Asset Allocation - April 2026

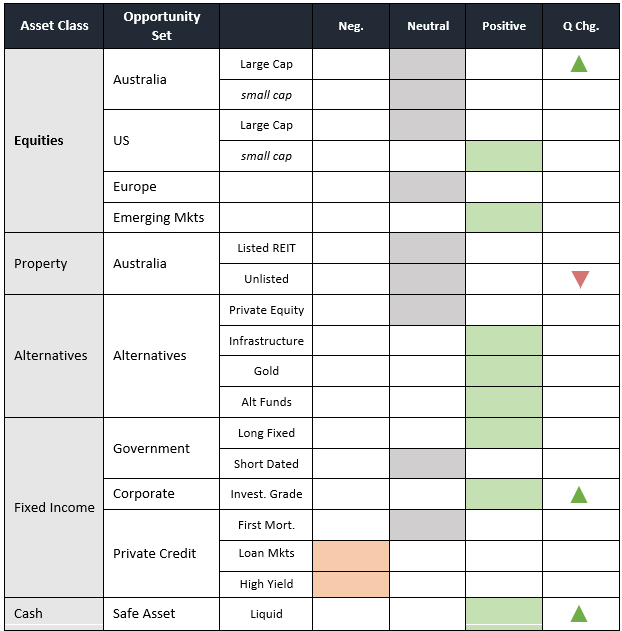

Tactical Allocation Calls (Quarterly view)

“ Predictions are Worthless – Predicting is Invaluable” – Peter Wurn

Thoughts

Australian Equities: A tough March for the ASX 200 at -7% and YTD at -1.6%. AI impacted Tech was down 28% ytd and down 8 months straight. As we write, there has been a rebound, but how resilient? As an open economy facing Hormuzian (sic) forces, we are exposed, but if recent $A behaviour is a guide, then we will see offshore support. We expect Resources to outperform Financials and selective value in the broader Industrials complex. Smalls Caps were smashed -11% in March, so again pockets of value with Resource stocks favoured. We raise to Neutral. An important Federal budget this month will shape our view on fiscal and monetary fronts.

US Equities: Not safe to take off the neck brace just yet. First the SaaS selloff, then Iran. On the latter, the market has undergone a geopolitical - not fundamental - selloff. Heightened geopolitical risk repriced the investor equity risk premium across the board. So, the sell off was a valuation story, not an earnings one. Earnings forecasts currently remain untouched – hence the sharp rebound. AI capex will now add 1% to US GDP – the war did not chase that away. The stimulatory BBB cheques have been posted. So, we retain our positive view and with the expensive Tech sector now better value. We hold both Large Cap and equal weighted exposure. With the fiscal stimulus and a lower USD, we retain current settings.

European Equities: Just when you thought it was safe to get back in the water the Iranian conflagration and has come along and highlighted strategic weaknesses in Europe’s energy structure If the Oil price falls to where futures markets are pricing, then we would expect a robust economic recovery. Watch.

Emerging Markets: A major beneficiary of the switch from the extended US markets until recent events. We expect markets to move inline with the ebbs and flows of the ME situation. Sans the current Iranian situation we are positive, but in the meantime sit at Neutral and allocate on planned long term settings.

Property: With rates backing up and (negative) interest rate cuts forecast, we step back to Neutral in both Listed and Unlisted. Not unduly concerned, but we see better value in allocating elsewhere.

Private Equity: A Private Equity negative illiquidity premium? All the hopes for a rejuvenated market for exits are now diminished. Saasapocolypse (sic), higher Interest rates and fewer exits are not helping sentiment. Choose your LPs wisely. Liquidity in semi-liquid structures should be monitored.

Infrastructure: Contrary to a rising interest rate backdrop, we remain positive here. As a portfolio diversifier and inflation hedge, we remain confident on solid returns.

Gold: We now see Gold entering into a broad consolidation phase. Longer term we are a buyer standing side-by-side with China. Currently, Silver is off the menu with our interest back at US$55.

Government Bonds: With a stagflationary inducing middle east war, markets are completing a handbrake turn from easing to tightening. Given positive correlations, are bonds now a better risk adjusted buy than equities? Lond Bonds locally at 5% are attractive though US rate pressures may push rates higher. O/weight.

Private Credit: Cockroaches rampant? Not quite yet. Spreads are widening as default rates rise closer to long term averages. We see this as a normalisation rather than systemic collapse. There will be juicy headlines about SaaS credit exposure, but concentrating in the investment grade market and with the right managers, investors will remain compensated for an improving risk environment and better pricing.

Cash: Overweight. Cash gives us “optionality” for deployment in volatile markets and returning 4%+, we are not being unduly penalised for being patient.

DAA Calls enclosed proposed are for general investment purposes. Please discuss with Carnbrea the suitability of any recommendation to portfolios and the context of client SAA construct, holdings, return analysis and tax consideration. This document has been prepared and issued by Carnbrea & Co Limited ABN 33 004 739 655 (‘Carnbrea’), Australian Financial Services Licence No 233763. Any advice included in this document is general in nature and does not consider your objectives, financial situation or needs. Before acting on the advice, you should consider whether it’s appropriate to you. If a product we recommend has a Product Disclosure Statement (PDS), you should read it before making a decision. Past performance is not a reliable indicator of future performance. Derivatives are leveraged products which means gains and losses are magnified, and you may lose substantially more than your initial investment. We do not endorse any information from research providers that we provide to you unless we specifically say so.

Copyright © | 2026 |Carnbrea & Co.| All rights reserved