Portfolio Construction Series - Part Two

Active vs Passive Asset Management - What to use when?

by Colin Campbell - Managing Director

When it comes to active vs. passive management strategies in our portfolio construction – we use both. It’s a “horses for courses” approach.

When do we use an ETF?

Fundamentally, we use an ETF where we cannot find a manager that we believe can offer, over time, a sustainable advantage in performance, net of fees, in the market which we want exposure to.

Oftentimes, this occurs because the underlying market is highly efficient, and after accounting for manager fees, the active manager tends to underperform compared to the available passive alternatives.

The decision for the adviser in choosing a Passive ETF

Some of the inputs to the adviser’s decision to use a passive ETF would include:

Is the underlying index (i.e. S&P 500) the best vehicle to represent the exposure I want my client to have in their portfolio?

How will it blend with other proposed investments to generate the right risk reward outcomes for the client?

Will it be cost effective?

Is there an Active manager who can do a better job than the ETF?

When do we use an ETF?

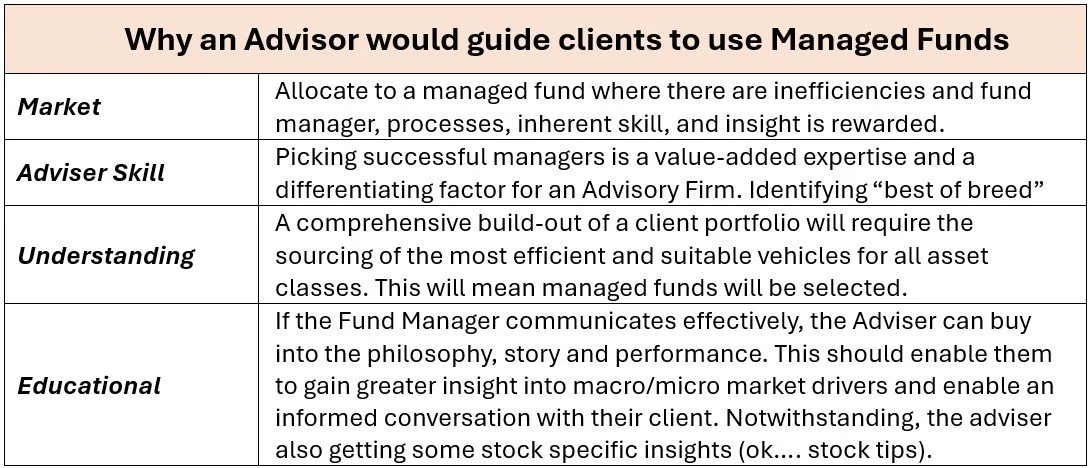

We use a Managed Fund where we believe that the Fund can have a greater chance of outperformance than an ETF, or where no quality ETF exists. Usually these are in markets which are less efficient i.e. small, illiquid, have limited coverage by analysts, have an idiosyncratic market structure etc – and more importantly, where a manager can genuinely apply skill in extracting value.

Core and Satellite

In the parlance of Core vs Satellite, we would expect ETFs to provide a large constituent part of the cost efficiency, diversification, tax efficiency and lower volatility etc. with actively managed funds or other direct investments driving the potential for blended outperformance.

The asset classes where we would potentially choose an active manager over an indexed fund are;

Core Markets

Developed Market Equities - where the manager has shown sustainable outperformance and often used alongside index replicating ETFs.

Government Bonds/Fixed Interest.

Satellite Markets

Small/Mid Cap Equities in Core markets

All Cap exposure in less mature equity markets outside of the Developed world.

Other Asset Classes

Private Credit

Hedge Funds

Private Equity

Infrastructure

Commodities

Property

Disclaimer: This information is provided by Carnbrea & Co Limited ABN 33 004 739 655, Australian Financial Services Licence No. 233763. Any advice included in this document is general in nature and does not take into account your objectives, financial situation or needs. Before acting on the advice, you should consider whether it is appropriate to you. If a product we recommend has a Product Disclosure Statement (PDS) or a Prospectus, you should read it before making a decision. Past performance is not a reliable indicator of future performance. Derivatives are leveraged products which means gains and losses are magnified and you may lose substantially more than your initial investment. We do not endorse any information from research providers that we provide to you, unless we specifically say so.